Table of Contents

During its 35th meeting, the GST Council resolved to establish an e-invoicing system that would apply to specific categories of individuals, primarily large enterprises. Subsequently, it was extended to encompass mid-sized and small enterprises.

This blog explains what e-invoicing is and how it works, its importance and the consequences of not complying with it to help organizations understand and execute it effectively.

What is e-invoicing?

The term “e-invoicing” refers to electronic invoicing as defined by the GST legislation. Just as an e-way bill is used when a business that is registered for GST transports products from one location to another similarly, some notified GST-registered companies are required to create electronic invoices for business-to-business (B2B) transactions.

‘e-Invoicing’ or ‘electronic invoicing’ refers to a system in which B2B invoices are electronically authorized by GSTN. E-invoicing does not imply generating invoices on the GST portal but instead submitting an already prepared standard invoice to the government e-invoicing portal, i.e. Invoice Registration Portal (IRP), and getting it verified by GSTN. As a result, it automates multi-purpose reporting with a single input of invoice information.

Who must generate the e-invoice and its applicability?

Earlier firms with a turnover of over Rs. 10 crores were liable to register for e-invoicing. However, CBIC recently extended e-invoicing to enterprises with a turnover of more than Rs 5 crore, effective from August 1, 2023.

The taxpayer must comply with the e-invoicing in the current financial year and onward if their Annual Aggregate Turnover (AATO) exceeds the specified limit (5 crores at present) in any financial year from 2017-18 till date.

Exception: Who does not need to comply with e-invoicing?

Irrespective of their AATO few entities do not need to comply with e-invoicing. Entities that need not comply with e-invoicing are listed below:

- An insurance, a bank, or a financial institution, including an NBFC.

- A Goods Transport Agency (GTA).

- A registered person who provides passenger transportation services.

- A registered person providing services by admission to the exhibition of cinematographic films at multiplexes.

- A Special Economic Zone (SEZ) Unit

- A government department and local authority (excluded under CBIC Notification No. 23/2021 – Central Tax)

- Persons registered under Rule 14 of CGST Rules (OIDAR)

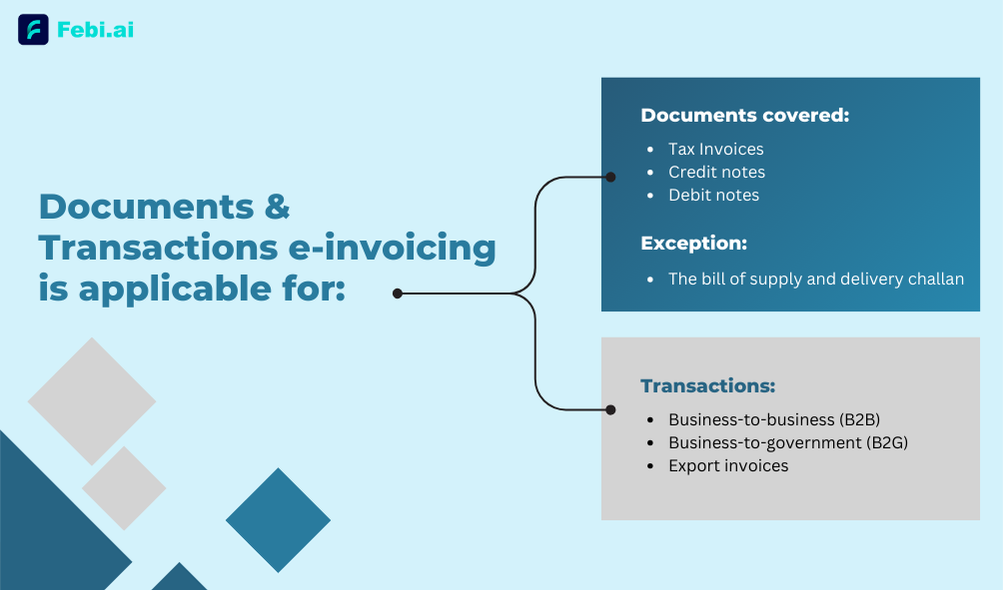

Documents and Transaction e-invoicing apply to?

E-invoicing is applicable to tax invoices, credit notes, and debit notes, except for the bill of supply and delivery challan.

In terms of transactions, e-invoices must be issued for all business-to-business (B2B), business-to-government (B2G), and export invoices. These transactions could be regular or reverse charge transactions.

What are the mandatory fields for invoices to be valid under e-invoice standards?

The e-invoice schema includes both necessary and optional fields. The necessary fields must be present for an invoice to be considered valid under the e-invoice standard. All essential fields should be filled out to register an e-invoice on the Invoice Registration Portal. A necessary field that contains no value can be reported as NIL.

The invoice can be divided into two parts – The invoice header section and the transaction section. A summary of the mandatory fields in each section is listed below:

Invoice Header Information

| Field Name | Description |

|---|---|

| Document Type | Defining whether the invoice is a tax invoice, credit note, debit note, or bill of supply. |

| Invoice Number | A unique differentiating code for tracking the invoice. |

| Invoice Date | The date of invoice generation. |

| Supplier Details | Name, address (with pincode) and GSTIN of the supplier. |

| Buyer Details | Name, address (with pincode) and GSTIN of the buyer. |

Transaction Details

| Field Name | Description |

|---|---|

| Product/Service Description | Details of the services or items provided. |

| Quantity & Unit Price | Number of goods or the hours of services provided, respectively, along with the price per unit or hour. |

| HSN/SAC Code | The specific code for the goods or services. |

| Subtotal Amount | Total cost of goods or services before taxes and additional charges. |

| Applicable Taxes | Specify the applicable GST rate along with the breakdown of the value of applicable taxes, including IGST, CGST, and SGST. |

| Total Invoice Amount | Total cost of goods with GST. |

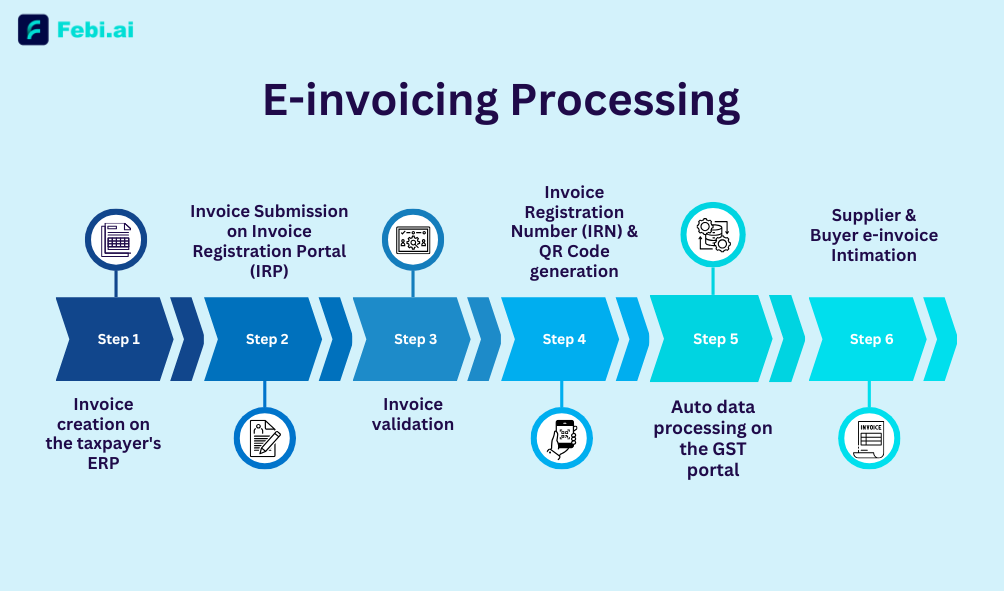

What is the e-invoicing process?

For creating or raising an e-invoice, numerous steps are performed, which are listed below:

Step 1 – Invoice creation on the taxpayer’s ERP

The taxpayer must generate a regular invoice using the respective ERP or billing software. Subsequently

Step 2 – Invoice Submission on Invoice Registration Portal (IRP)

Upload the invoice onto the IRP either using the JSON file, an application service provider (app or GSP), or a direct API.

Step 3 – Invoice validation

Once the invoice is uploaded on IRP, it will authenticate the B2B invoice’s essential details and check for duplicates.

Step 4 – Invoice Registration Number (IRN) & QR Code generation

Once the invoice is validated, IRP generates the invoice reference number (IRN) or hash for future reference, digitally signs the invoice and generates a unique QR code along with the acknowledgement number and acknowledgement date in JSON for the supplier.

The IRN is produced based on four parameters: the seller’s GSTIN, the invoice number, the fiscal year (YYYY-YY), and the document type.

The QR code will allow for quick display, validation, and access to invoices via devices. The QR code consists of the following parameters:

- Supplier GSTIN

- Recipient GSTIN

- Supplier’s invoice number

- The date of the generation of the invoice

- The invoice value (taxable value and gross tax amount)

- The number of line items

- The HSN code of the main items (the line item having the highest taxable values)

- The unique IRN (hash)

Step 5 – Auto data processing on the GST portal

The signed e-invoice data will be submitted to the GST system, where the supplier’s GSTR-1 and the buyer’s GSTR-2B/2A will be updated depending on the information provided in the invoice. Where applicable, invoice details will be used to amend ‘Part A’ of the E-Way Bill. As a result, just the vehicle number must be entered into ‘Part B’ of the E-Way Bill system to generate an E-Way bill.

Step-6 – Supplier & buyer e-invoice intimation

Now, the authenticated and digitally signed e-invoice is sent back to the supplier, which the supplier shares with the buyer.

Benefits of e-invoicing to business?

The following are the benefits businesses enjoy by using e-invoicing initiated by GSTN:

- E-invoice closes a significant gap in GST data reconciliation by eliminating mismatch errors.

- E-invoices made with one software can be read by another, increasing interoperability and reducing data entry errors.

- The e-invoice allows for the real-time monitoring of invoices created by the supplier.

- Automation of the GST return filing process allows the relevant invoice details to be automatically filled in across different returns, particularly when creating part of e-way bills.

- The possibility of tax authorities conducting audits is reduced due to the fact that the information they require is accessible at the transaction level.

How can e-invoicing curb tax evasion?

In the following ways, e-invoicing aids in reducing tax evasion:

- Since the e-invoice must be generated through the GST system, tax officials will have real-time access to transactions as they occur.

- Since the invoice is created before a transaction is completed, there will be less room for invoice manipulation.

- Since all invoices must be created via the GST system, it will lessen the possibility of fraudulent GST invoices and allow only legitimate input tax credits to be claimed.

- It is simpler for GSTN to detect fraudulent tax credit claims since the input credit may be compared to output tax information.

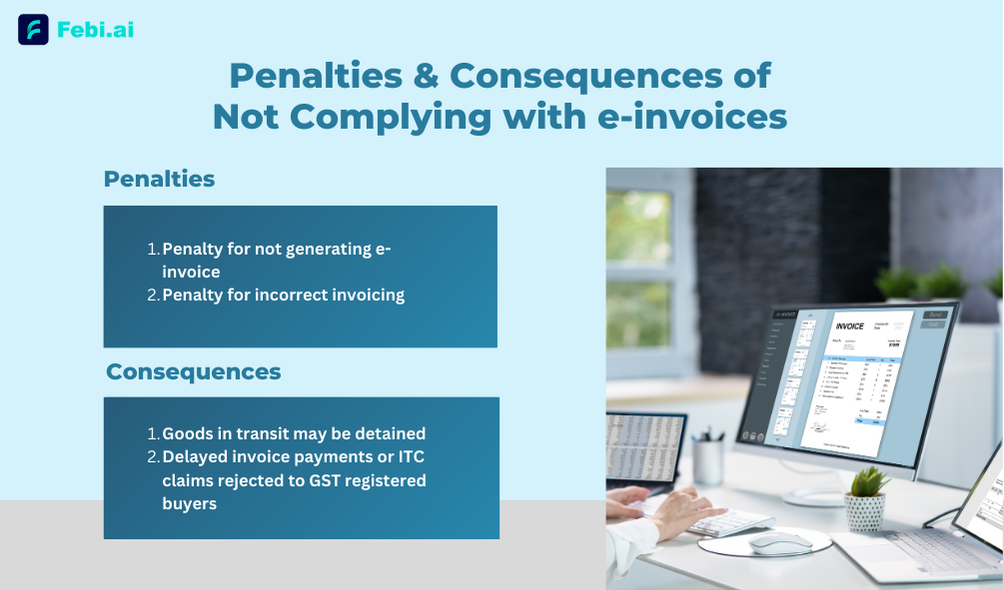

What are the penalties & consequences of not complying with e-invoices?

Taxpayers who meet the annual aggregate turnover criteria and supply taxable goods/services are required to notify the government of all B2B/B2G/export supply transactions by uploading invoices on the Invoice Registration Portal. The failure to generate e-invoices implies that supply transactions will not be reported to the government. Any invoice submitted by the applicable taxpayer that does not include the IRN is considered invalid under GST law. In other words, it is regarded as a non-issue of the invoice. As a result, failing to generate an e-invoice invites penalties.

The penalties for non-compliance with e-invoice are stated below:

- Penalty for not generating e-invoice – 100% of the tax due or Rs.10,000, whichever is higher, for every invoice.

- Penalty for incorrect invoicing – Rs.25,000 per invoice.

Along with the penalties, non-compliance leads to several consequences, some of which are outlined below:

- Goods in transit may be detained

The transportation of goods without an e-way bill and an e-invoice is not valid. It can result in the detention of transportation of goods. Since an invoice without an IRN and a signed QR code is invalid wherever applicable, transportation leads to goods and vehicle detention, which attracts the standard penalty for an e-way bill. - Delayed invoice payments or ITC claims rejected by GST-registered buyers

According to GST rules, a tax invoice is required to claim the Input Tax Credit (ITC). If a registered buyer has an invalid invoice without an IRN and a signed QR code, the buyer may refuse to accept delivery of goods or refuse to make payment, which will affect and delay the buyer’s eligibility to claim ITC.Technically speaking, an invoice that does not include an IRN cannot be auto-populated into the supplier’s GSTR-1 and may never appear in the buyer’s GSTR-2A and GSTR-2B. The buyer cannot claim the amount as ITC if the provider has not deposited the tax with the government.