Table of Contents

Blockchain, with its revolutionary advancements in data security, transparency, automation, and auditability has the potential to completely transform accounting procedures. It is changing the accounting landscape across industries, from enabling real-time reconciliation to creating unchangeable audit trails.

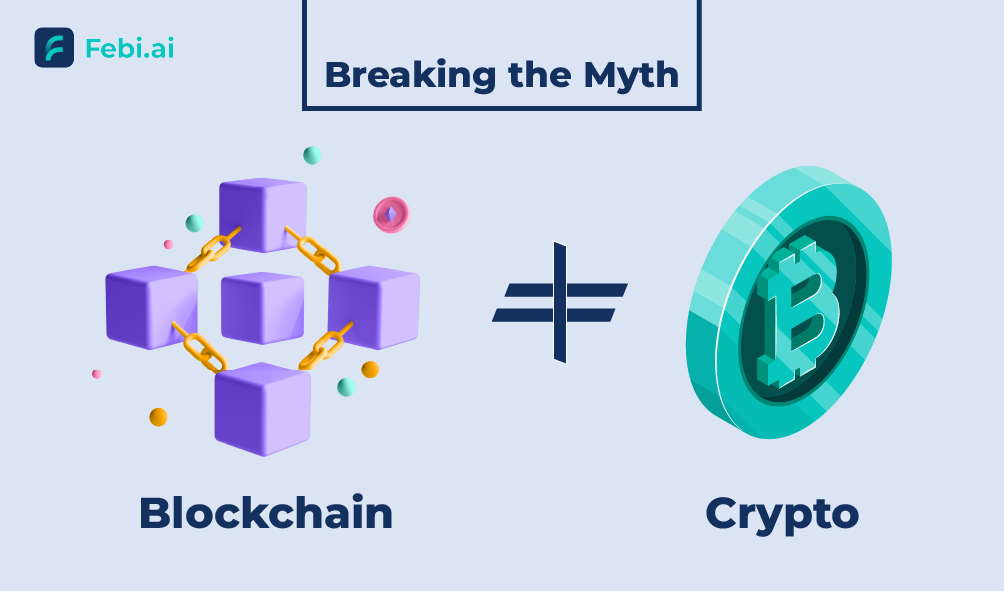

Normally, when people hear the word blockchain, they immediately associate it with cryptocurrencies like bitcoin. Although blockchain serves as the foundation for cryptocurrency assets, its true potential goes well beyond virtual money, especially in the context of modern accounting.

This blog will explore how the concept of blockchain is so much more than just its association with cryptocurrency.

Breaking the Myth: Blockchain ≠ Crypto

Blockchain, in the simplest terms, refers to a distributed ledger that securely and openly documents data exchanges or transactions. One of its key features is being decentralized, and consequently, cryptocurrency is just a singular application of it.

Some other potent features of blockchain are:

- Immutable – once it is recorded, it cannot be altered or edited.

- Distributed – it is also shared amongst multiple participants in the network.

- Transparent – it is accessible for verification when needed.

Therefore, whether or not cryptocurrency is involved, these features have significant ramifications for the way transactions are recorded, validated, and audited.

Immutable Audit Trails and Tamperproof Records

In accounting, one of the biggest challenges is maintaining the integrity of data. Meaning, ensuring that no one has deleted the data recorded or tampered with the changes. Blockchain helps maintain this security by time-stamping each transaction and cryptographically sealing it, making the entries immutable, and creating a chronological and permanent record of them to track them in a sequence.

By properly following these measures, we are reducing the risk of fraud or manipulation, improving audit readiness, while ensuring all changes are traceable and verifiable. All in all, this will result in more accurate and quick reviews, while also reducing the manual effort needed to check the authenticity of the records.

Real World Use Cases

1. Smart Contracts

Smart contracts are agreements that run on their own and are written directly into a blockchain’s code. In accounting, these play an imperative role as it can help reduce human error, time taken, and any confusion in financial transactions. This is possible because it automates revenue recognition when predefined conditions are met, creates invoice upon delivery confirmations, and maintains contractual compliance without any manual intervention.

2. Real Time Auditing

Blockchain also allows continual, real time auditing by providing auditors access to an immutable ledger, whereas traditional audits primarily rely on periodic reviews and sampling. Consequently, blockchain helps reduce the time and cost taken to audit, identify any anomalies, and drastically increases confidence in compliance and reporting.

3. Intercompany Reconciliation

Blockchain allows the transaction data to be concurrently updated across the network, making reconciliation almost instantaneous, thereby reducing any discrepancies or delays. It makes the entire process a lot less time consuming and helps minimise human errors effectively.

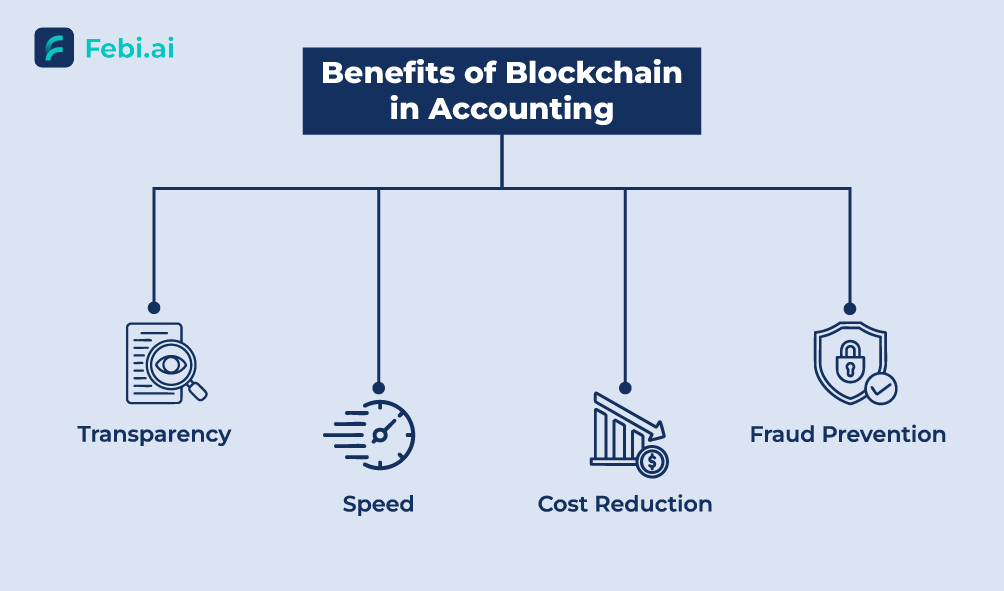

Benefits of Blockchain in Accounting

Blockchain is highly advantageous when employed for accounting. Some of its key benefits are:

- Transparency: Through blockchain all stakeholders are allowed to access the same set of records, reducing any disputes and improving confidence in one another.

- Speed: It helps automate aspects of accounting like journal entries and reconciliations, improving not just how quickly these are performed, but also the efficiency of the organization.

- Cost reduction: Since blockchain reduces the need for manual labour, there is a reduction in the operation cost.

- Fraud prevention: It basically makes it impossible to change records without it being detected, decreasing the risk of internal or external risk.

Challenges of Modern Accounting With Blockchain

- Scalability – Organizations with blockchain networks can face performance bottlenecks with high volumes of transactions. This can lead to a slower process and a higher cost.

- Standardization – Since there aren’t any standard regulations to follow for the integration of blockchains, it creates inconsistent results and complicated adoptability.

- Regulatory considerations – Regulators have not yet entirely grasped the capabilities of blockchain and accounting, therefore there is still uncertainty as to how they might respond to its features like smart contracts, decentralized ledgers and more.

Future Potential of Blockchain in Audit and Compliance

The future of blockchain is highly promising, as it presents us with the ability to create tamperproof and verifiable records. This is ensuring that the organizations are able to take full advantage of regulatory compliance, audit automation, tax reporting, digital identity verification, and anti-money laundering (AML) processes. Hence, if it continues to move at its current pace, it might soon become part of the core infrastructure for modern accounting, and reshape it to greater heights.

Conclusion

From static, retroactive documentation to ever-changing, real-time financial ecosystems, blockchain indicates an evolutionary shift in accounting. It provides previously unheard-of levels of precision, speed, and trust that legacy systems just are unable to match.

Though there are still obstacles to overcome, progressive companies and accountants are already investigating how blockchain technology can be used to automate essential procedures, lower fraud, as well as streamline compliance.

Blockchain might eventually establish itself as fundamental to finance as double-entry bookkeeping did, bringing about a new era of operational efficiency and financial transparency.