Even a small miscalculation or errors can result in costly consequences and legal issues. This is probably why even the most experienced business owners and entrepreneurs experience stress and anxiety during the tax season. Do you, too, fear the tax season and try to balance it all without making any mistakes? Are you overworked about managing compliance in tax, right business tax return or say your company tax return?

Whether you are a seasoned businessman or a new startup enthusiast, we have curated a detailed list of the 10 most common mistakes you should keep in mind at the time of business tax filing. This will help you avoid compliance issues and paying unnecessary fines and penalties, keeping your financial operations running smooth and compliant always.

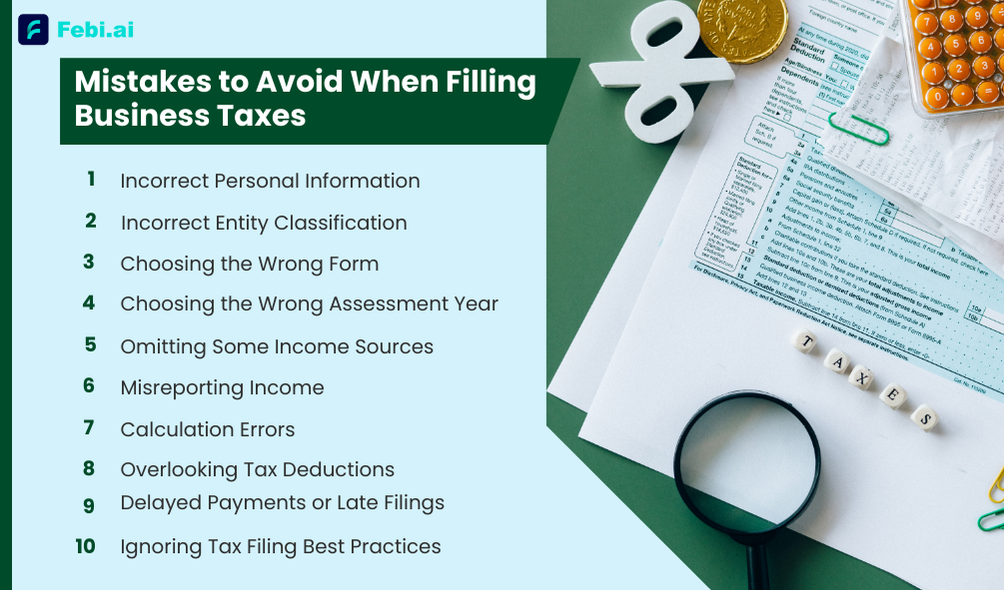

1. Incorrect Personal Information

Adding or sharing incorrect personal data is one of the most common tax filing errors in filing business and personal taxes. Several business tax payers make inaccuracies in their name, PAN number, company name, or business address.

Doing such basic mistakes, or rather typos can result in processing delays or even make the authorities reject your tax return. To avoid such problems, it’s recommended to always double-check all personal information before you submit your tax documents. This will ensure that all data matches your records, with the one shared for the taxes.

2. Incorrect Entity Classification

“I selected the wrong business entity on my tax return”. This is another business tax mistake made by people when filing taxes for their company financials. No matter whether you are a sole proprietor, running a business in partnership, LLC, or a corporation, you need to know that every entity has its own, distinct tax requirements.

In case you file the taxes for a wrong entity, there shall be improper tax treatment, which would further result in unnecessary fines and penalties, affecting your business cash flow. To avoid these problems, crosscheck your business structure and ensure you’re using the appropriate classification of your business on the forms to stay tax compliant.

3. Choosing the Wrong Form

A lot of taxpayers are guilty of choosing the incorrect tax form for their business types, resulting in filing errors and missed opportunities for their income tax deductions/ deducted tax. For example, sole proprietors, self-employed individuals and entrepreneurs need to report their income within the “Income from Business or Profession” head when filing the ITR.

On the other hand, proprietors, partnership firms and LLPs need to use the ITR-5 to file their returns. Similarly, private limited companies need to use the ITR-6. Familiarize yourself with the appropriate forms for your business type to avoid errors and ensure accurate reporting.

4. Choosing the Wrong Assessment Year

A lot of people are still confused between assessment year and financial year. And this is the major reason behind taxpayers choosing the wrong assessment year. Incorrect assessment year can create significant problems in your tax return. To avoid tax penalties, you must carefully review all documents and so you will report income and expenses for the right assessment year.

5. Omitting Some Income Sources

The Section 56 of the Income Tax (IT) Act, 1961 states that “Income from other sources” are considered as earnings which don’t fall within any income head. Most tax payers in India are unaware of this and so avoid mentioning the income from other sources within the correct head when filing for their tax returns.

Let’s look at a practical example to understand this better.

Assuming a person’s annual income from savings is less than INR 10,000, they are not eligible to pay taxes. But think of another scenario wherein their earned interest income of INR 15000 in the same year. In this case, INR 15000 of interest shall fall within the ‘Income from other sources’ head and on this you can claim deductions as per the Section 80TTA.

It’s important to note that this is valid if your age is less than 60 years.

To avoid this error, maintain a detailed record of all income streams, such as side gigs, consultation, investments and secondary business activities that generate income and ensure that every single rupee is accounted for in your tax filings.

6. Misreporting Income

This is one of the most common concerns or errors faced by entrepreneurs or finance managers. Over-reporting, underreporting, or misreporting income can lead to serious tax consequences, including fines and audits. Overreporting may cause you to pay more taxes than necessary, while underreporting can lead to penalties. Use accurate financial statements and double-check each and every entry so your reported income is accurate.

7. Calculation Errors

Simple miscalculations can cause significant problems in your tax return, affecting the accuracy of your total tax liability. These errors can lead to incorrect tax payments or missed opportunities for deductions. To avoid this issue, it’s best to utilize reliable accounting software that helps you avoid miscalculations and ensure accurate reporting.

8. Overlooking Tax Deductions

A lot of business owners and entrepreneurs skip valuable business tax deductions as they may be unaware, causing a significant effect on your taxable income. For example, expenses relevant to home office use or your business travel expenses can be left overlooked. When filing for your taxes, make sure you are well educated and informed about all existing deductions for your business and this shall directly help you increase your savings.

9. Delayed Payments or Late Filings

Failing to timely pay your taxes or overrunning the final filing deadline can result in severe fines and penalties and add interest charge liability to your expenses. To avoid facing this issue, be aware of due and pending tax compliance deadlines. You can even set reminders to avoid these issues.

10. Ignoring Tax Filing Best Practices

Ignoring established tax filing best practices can lead to a host of problems, from inaccuracies to compliance issues. Regularly update yourself on tax laws and regulations and consider consulting a tax professional for guidance. Adhering to best practices helps ensure that your tax filings are accurate, compliant and efficient.

Table of Contents

How to Avoid these Mistakes in GST Compliance for Your Business

Tackling and managing the world of business tax compliance/GST compliance and filing doesn’t have to be stressful. By educating yourself of these common mistakes and taking mindful steps to avoid them, you can save yourself from unnecessary stress and potential penalties. Remember, meticulous attention to detail and adherence to best practices are key to successful tax filing. So, embrace these tips and file your taxes with confidence, ensuring that your business remains in good standing with tax authorities. Remember, a little preparation and staying informed can go a long way in keeping your business finances shipshape and maximizing your tax benefits.

Filing taxes can be complex and time-consuming, but Febi.ai simplifies this process effortlessly. India’s first AI-powered platform, Febi manages your business recording through automated bookkeeping in real time. It also provides a dynamic GST compliance/TDS compliance calendar on your personalized dashboard that shows all paid, due and pending tax compliance dates with the accurate amounts for your business.

Ready to see how Febi.ai can streamline your tax compliance, bookkeeping and financial reporting? Schedule a live demo today and experience its capabilities first-hand to discover how it can transform your financial management.