Table of Contents

Introduction

Running a small business is exciting, but let’s be honest – taxes often feel like a maze. Between filing returns, figuring out deductions, and staying on top of compliance, it’s easy to feel buried. That’s where tax optimization steps in. It’s not about dodging taxes; it’s about being smart so your business only pays what it truly owes – nothing extra. For those just starting out, tax planning for new business can set a strong financial base that lasts for years.

Understanding Tax Optimization

At its core, tax optimization is about arranging your finances in a way that reduces taxes – legally. It means playing by the rules, but playing smart. There’s a big difference here: tax evasion? That’s illegal and risky. Tax planning? That’s just good business sense.

Why Tax Optimization Matters for Small Business Owners

If you’re running a business, you know every rupee matters. A thoughtful tax plan doesn’t just save you money – it frees up cash for growth. Even saving 5-10% in taxes could fund a new hire, marketing push, or fresh equipment. And honestly, the relief of not dreading surprise penalties? That’s priceless.

Using the right tax reduction techniques for entrepreneurs means you’re not overpaying, and you’re still staying fully compliant.

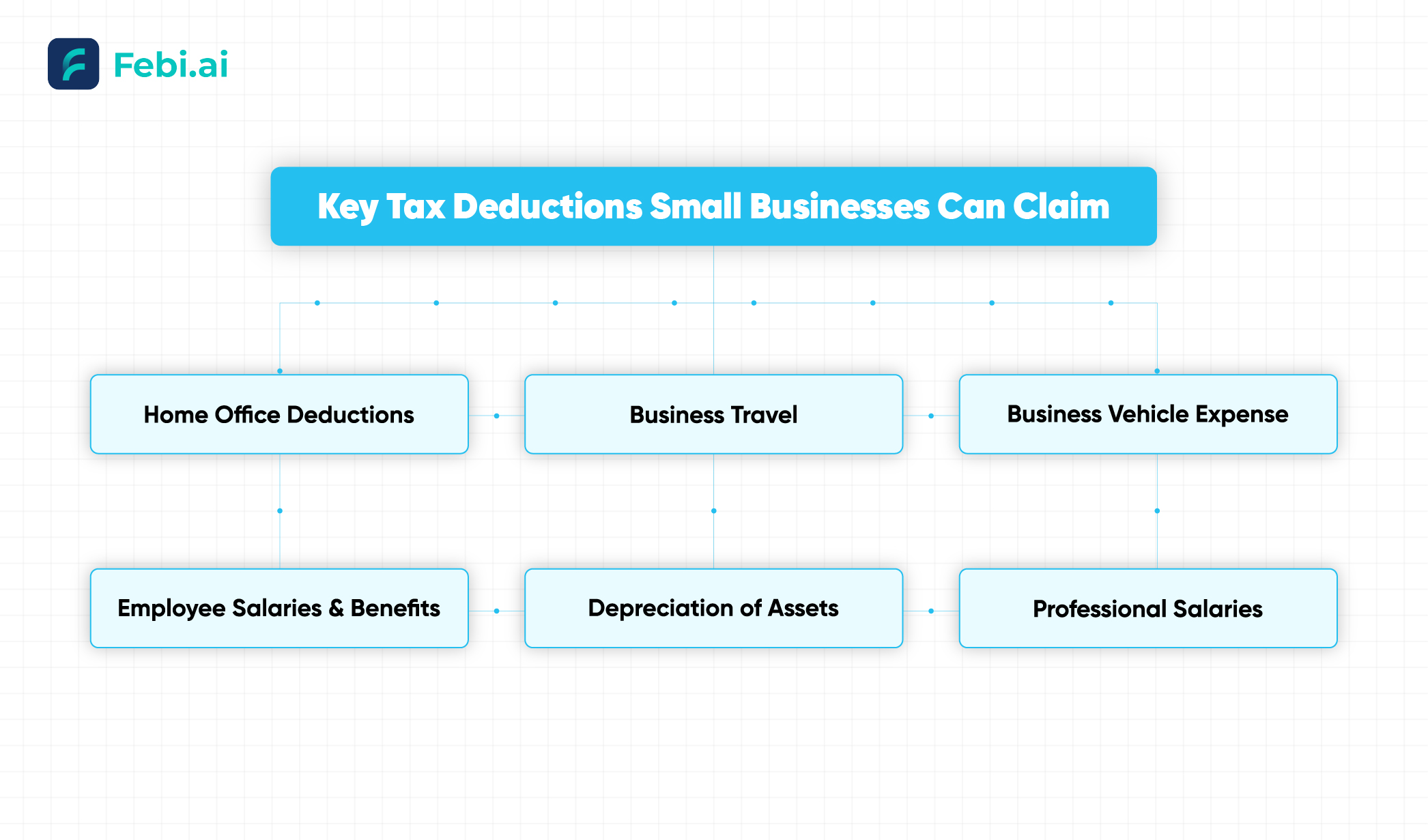

Key Tax Deductions Small Businesses Can Claim

Deductions are at the heart of small business tax saving strategies. Here are some worth tracking:

- Home Office Deduction – If you use a part of your home just for business, you can deduct a portion of rent, utilities, and internet.

- Business Travel & Vehicle Expenses – Think fuel, lodging, meals, or tolls; they reduce your taxable income.

- Employee Salaries & Benefits – Wages, insurance, and retirement plans are all deductible.

- Depreciation of Assets – Furniture, laptops, and delivery vehicles lose value, and you can claim that depreciation.

- Professional Services – Fees for accountants, legal experts, marketing agencies and consultants all count.

Applying these consistently is one of the strongest tax strategies for small business owners.

Structuring Your Business for Tax Efficiency

The business structure you choose shapes how much tax you pay. A sole proprietorship is simple, but you’ll be taxed at personal income rates. Partnerships and LLPs spread the income, lowering the burden. Private limited companies may enjoy lower corporate rates, though compliance is tighter.

It’s not about copying others – it’s about picking what aligns with your growth path. A freelancer may find sole proprietorship easy, while a scaling agency might save more as an LLP. Truth is many smart tax strategies for small business owners start right with the structure.

Utilizing Tax Credits Available for Small Businesses

While deductions lower income, credits directly cut your tax bill. Think of them like discounts applied at checkout. Some worth exploring:

- R&D Credits – For businesses investing in new products or processes.

- Hiring Credits – Incentives for employing people from specific categories.

- Startup Incentives – Benefits aimed at new businesses.

So many owners miss these simply because they don’t know they exist. That’s why getting advice pays off – you don’t want to leave free money sitting there.

Managing Expenses Strategically

A lot of owners lose tax benefits just by sloppy record-keeping. The key? Be consistent.

- Log every single expense, even coffee meetings or software tools.

- Keep personal and business costs separate – mixing them just invites problems.

- Use cloud tools to automate tracking and categorizing.

It might feel simple, but this is one of the most powerful tax reduction techniques for entrepreneurs.

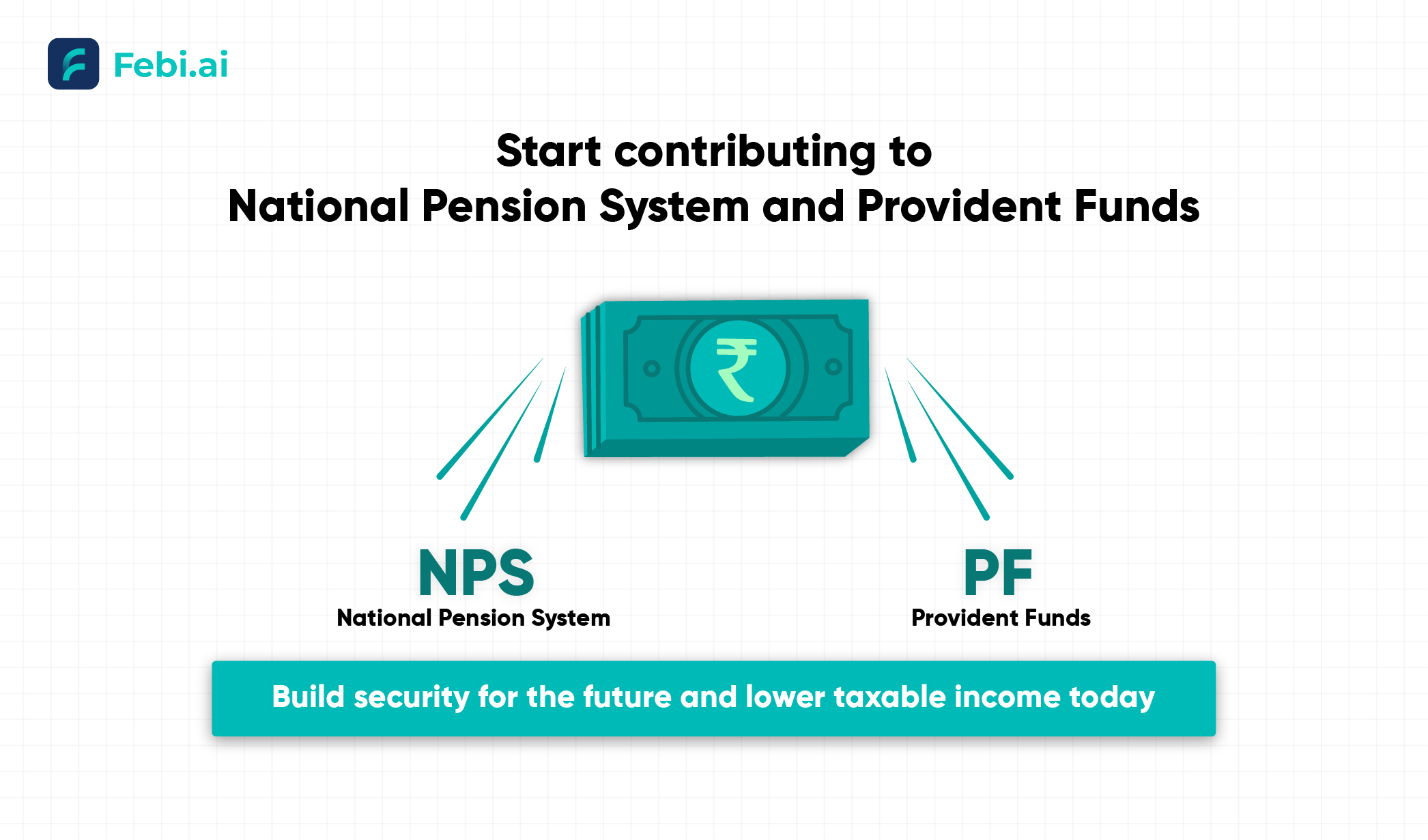

Retirement Planning as a Tax Strategy

Here’s a strategy many skip: retirement savings. Contributions to NPS or provident funds don’t just build security for the future – they lower taxable income today. For small business owners without corporate perks, this dual benefit is a no-brainer.

Depreciation and Capital Investment Planning

Buying assets like equipment or vehicles isn’t just about operations – it’s also about tax benefits. Depreciation lets you spread the cost over years, lowering profits (and taxes) steadily. Timing your purchases strategically can balance your tax outgo and improve efficiency.

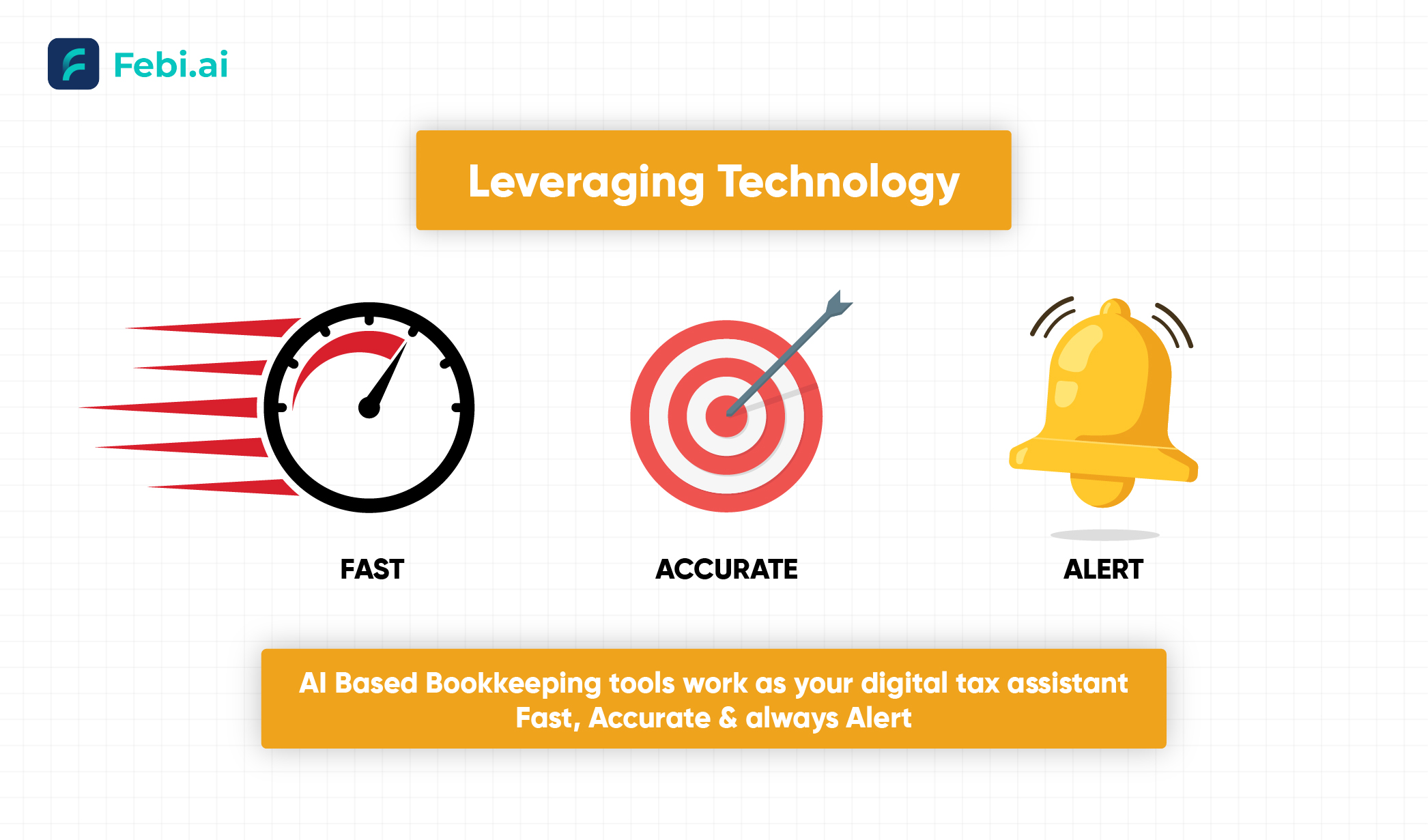

Leveraging Technology for Tax Optimization

Gone are the days of manual tracking. Cloud platforms and AI-based bookkeeping tools help capture expenses automatically, point out deductions you might overlook, and keep you compliant. Think of them as your digital tax assistant – fast, accurate, and always alert.

Tax Planning vs Tax Preparation

Here’s the difference:

- Tax preparation is end-of-year: filing returns, organizing receipts.

- Tax planning happens all year – making choices that save you money.

Especially for tax planning for new business, this difference matters a lot. Wait until the end, and you’ll likely miss golden opportunities.

Industry-Specific Tax Optimization Tips

Not all businesses are alike. Tailored tax strategies matter.

- Freelancers – Deduct laptops, internet, workspace.

- Retailers – Track stock accurately to manage profits and deductions.

- Service Providers – Claim training, tools, even client entertainment.

Customizing tax strategies for small business owners ensures you unlock savings generic plans miss.

Common Mistakes Small Business Owners Make

Plenty of mistakes repeat across businesses:

- Sloppy financial records.

- Missing deadlines, leading to penalties.

- Merging personal and business expenses.

- Skipping professional advice to save money.

Avoiding these is one of the easiest small business tax saving strategies.

Working with Tax Professionals

Hiring a CA or advisor isn’t a cost – it’s an investment. They know the law, catch deductions, and keep you safe from compliance headaches. For growth-focused businesses, outsourcing tax and accounting frees you up to focus on scaling.

Conclusion

Taxes don’t have to feel like a weight. With the right mix of deductions, credits, structure, and planning, they can become opportunities instead of obstacles. The aim isn’t avoiding taxes – it’s paying only what’s truly due and save whatever possible.

Whether you’re just starting out and focusing on tax planning for new business or running an established firm, the right tax strategies for small business owners can flip stress into stability. By embracing small business tax saving strategies and smart tax reduction techniques for entrepreneurs, you create financial breathing room – and that’s how businesses grow.