In the bustling world of business, especially for those who extend credit, bad debt expense is something you’ll inevitably encounter. Think of it as the financial hiccup that comes from sales you’ve made on credit, but where customers don’t end up paying. Understanding this aspect is more than just an accounting necessity—it’s key to keeping your financial statements accurate and your business decisions on point.

Numbers show that companies have written-off an average of about £40,000 in the unpaid invoices last year. This went up from an average of £17,500, only a few months back. This rise defines a 40% high in non-payments across the United Kingdom. Cleary, it’s a pressing concern across businesses, industries and geographical borders.

Table of Contents

Why Should You Care About Bad Debt Expenses?

Bad debt expense isn’t just another line item on your balance sheet; it’s an important determinant of your company’s financial health.

When you grasp how to calculate and manage this expense, you’re not just keeping your books in check—you’re also making sure you’re not overestimating how much you actually have coming in. This insight helps you make smarter, more informed decisions about your business’s future.

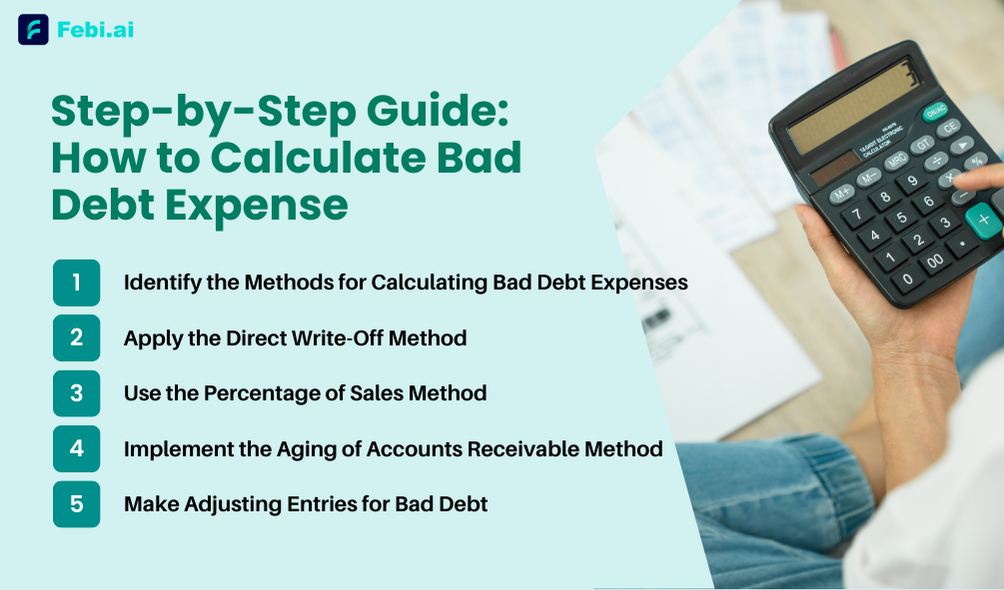

Step-by-Step Guide: How to Calculate Bad Debt Expense

1. Identify the Methods for Calculating Bad Debt Expenses

You’ll find multiple methods for bad debt expense calculation that you can choose from depending upon one each suited to different business needs and accounting practices. Some of the most opted options include:

- Direct Write-Off Method: This method involves writing off bad debts as they occur, directly reducing accounts receivable.

- Percentage of Sales Method: Estimates bad debt expense based on a fixed percentage of total credit sales.

- Aging of Accounts Receivable: Analyzes outstanding receivables based on their age and applies different percentages of uncollectibility.

2. Apply the Direct Write-Off Method

The Direct Write-Off Method is straightforward: you record bad debt expense only when a specific receivable is confirmed to be uncollectible. For instance, if a customer fails to pay a ₹10,000 invoice, you’d handle it like this:

Debit Bad Debt Expense ₹10,000

Credit Accounts Receivable ₹10,000

This method is simple and easy to understand, but keep in mind it doesn’t align with the matching principle of accrual accounting. This means it might not always reflect the true financial picture, as the expense is recorded only when the debt is deemed uncollectible.

3. Use the Percentage of Sales Method

With the Percentage of Sales Method, you can estimate the bad debt expense based on a percentage of your credit sales. Let’s try to understand this better with the help of an example. If you anticipate that 2% of your ₹50,000 in credit sales will be uncollectible, you calculate it like this:

Bad Debt Expense = ₹50,000 × 0.02 = ₹1,000

You would then record this ₹1,000 as an expense and adjust the Allowance for Doubtful Accounts to reflect this estimate. This method helps you better match expenses with the revenues they relate to, providing a clearer picture of your financial health.

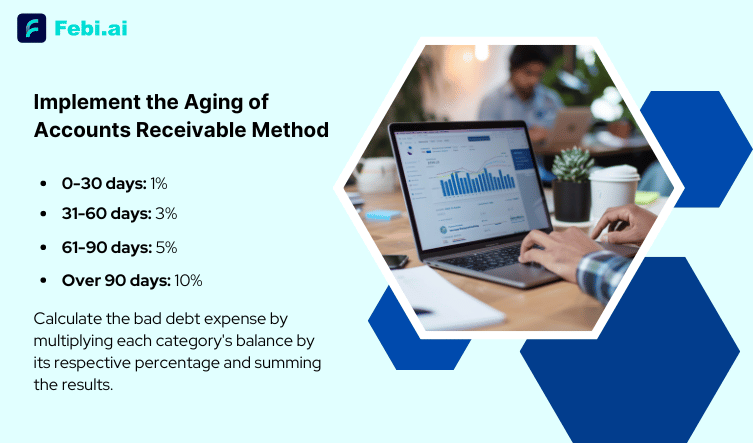

4. Implement the Aging of Accounts Receivable Method

It’s quite important to categorize accounts receivables based on how long they have been outstanding. For this, you need to apply different percentages of uncollectible amounts relevant to each category. For example, you could use this:

| Number of Days | Percentage |

|---|---|

| 0-30 days | 1% |

| 31-60 days | 3% |

| 61-90 days | 5% |

| Over 90 days | 10% |

Calculate the bad debt expense by multiplying each category’s balance by its respective percentage and summing the results.

5. Make Adjusting Entries for Bad Debt

At the end of each accounting period, adjust the allowance for doubtful accounts to reflect estimated uncollectible receivables.

Record the following journal entry:

Debit Bad Debt Expense for the estimated uncollectible amount.

Credit Allowance for Doubtful Accounts for the same amount.

Advantages of Calculating Bad Debt Expenses

Thinking about making a provision for bad debts in your business? Here are some of the top reasons why you should get to it at the earliest.

Improved Financial Accuracy

This is the leading benefit associated with accurate calculation of the bad debt expense calculation, as you get financial statements that truly reflect receivable values. Not only that but it also enhances their reliability and transparency. This accuracy is crucial for investors, creditors, and management to make informed decisions based on the company’s financial health.

Enhanced Decision-Making

Understanding your company’s or client’s bad debt trends helps make informed credit policies and manage all risks effectively, contributing to better financial health. This knowledge allows companies to adjust their credit terms and collection practices to minimize future bad debts.

Compliance with Accounting Standards

Regularly estimating and recording bad debt expenses ensures compliance with accounting standards in your country. Compliance with these standards is essential for maintaining credibility with the stakeholders and avoiding legal penalties.

Disadvantages of Calculating Bad Debt Expenses

Estimation Challenges

Estimating bad debt expense isn’t an exact science. It involves a lot of judgment and dealing with uncertainty, especially when trying to predict which customers might default on their payments.

This process can be tricky—if not done carefully, it can lead to inaccurate numbers that mess with a company’s financial picture. And when the numbers aren’t right, it can affect everything from day-to-day decisions to long-term business strategies, not to mention potentially misleading investors.

Potential Overestimation

If a company overestimates its bad debt, it could end up setting aside more money than needed to cover potential losses. This can make the company look less healthy than it actually is. Plus, a more conservative estimate could mean there’s less money available for reinvestment or pursuing growth opportunities, which can hinder the company’s ability to move forward.

Resource Intensive

Accurately tracking and estimating bad debt takes a lot of time and effort, especially when you’re dealing with a large number of customers. For bigger companies, this can be a huge task, often requiring dedicated teams and advanced software just to keep everything in line.

It’s a lot of work, and it can tie up resources that might otherwise be used for other important financial tasks, slowing down the overall efficiency of the business.

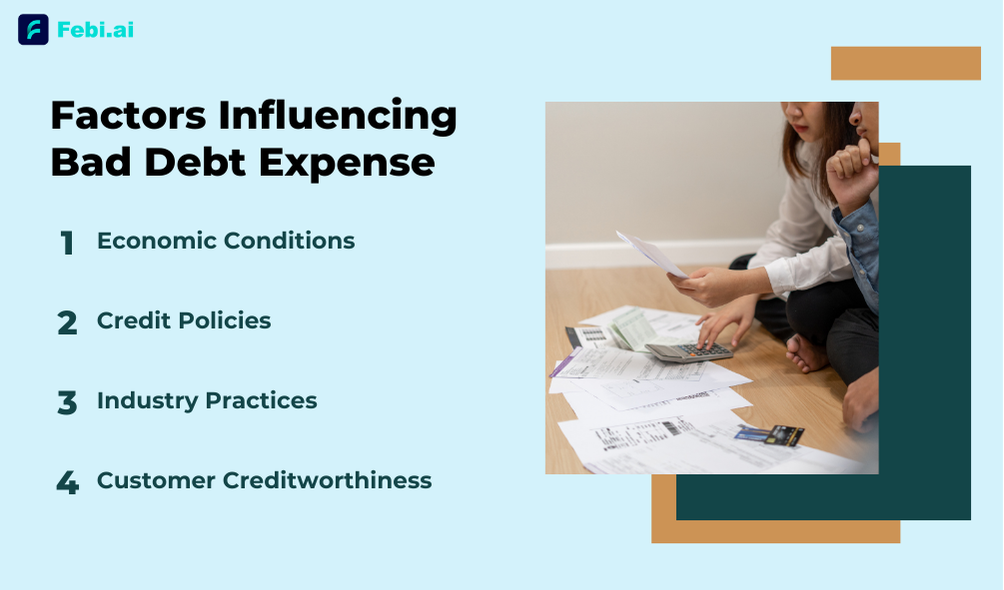

Factors Influencing Bad Debt Expense

When dealing with an AR account, bad debts are the undesirables of any business but you may be surprised to learn that there are several internal and external factors that add up to your bad debt expenditure.

Internal factors include weak credit supervision and administration systems, fraud incurred at the time of credit implementation workflow and overlooking of established processes by the employees dealing with credit. Here’s a list of some of the most stressing concerns that affect your organisation’s bad debts expense:

Economic Conditions

Economic conditions are inevitable and unfortunately, out of your direct control. But it’s commonly seen that economic downturns can increase the likelihood of customer defaults, leading to higher bad debt expenses. Conversely, a strong economy might result in lower bad debt levels.

Credit Policies

When doing business, it’s common to want to have lenient policies in place so as to encourage higher sales. But before you notice it, lax credit policies may result in higher sales but also increase the risk of uncollectible accounts.

This directly impacts your bad debts expense totals. The best way to approach this challenge is to impose stricter credit policies that may help you reduce bad debt. But make sure they are well balanced so it also doesn’t limit your sales growth.

Industry Practices

Different industries have varying norms for credit sales and collections, influencing bad debt expense patterns. Understanding industry benchmarks helps in setting realistic expectations for bad debt.

Customer Creditworthiness

It is critical to learn and identify if the person you are offering product or services on credit has has a positive payment track record. In this financial term this is called “credit worthiness”. When lending a loan, banks and financial institutions too, assess the creditworthiness of the individual.

The financial health and payment history of customers play a crucial role in determining the likelihood of bad debts. Regular credit checks and monitoring can mitigate the risk of extending credit to unreliable customers.

Mastering Bad Debt Expense for Financial Stability

We hope this blog helped you understand how to calculate bad debt expenses for your business or client’s. You’d have realised by now that accurate bad debt expense calculation is quite critical for maintaining financial health and stability in any business. As you understand the various methods and their applications for calculating business bad debts, you can better manage the receivables and mitigate the impact of uncollectible accounts, if any.

Whether you are a small business owner or a financial professional, mastering bad debt expense calculation lets you make more informed decisions and improve the overall financial reporting.