Picture this–You’re running a successful business, everything is going smoothly until it’s time to handle your GST returns. GSTR-1, a crucial part of this process, might seem intimidating at first, but it’s essential for every registered taxable person. This return captures all your outward supplies of goods and services, ensuring that the sales data of your business is transparent and accountable.

But what makes GSTR-1 so important? It plays an important role in the reconciliation of input tax credit (ITC). By filing of GSTR-1, you make your sales data available to your buyers, allowing them to claim ITC without a hitch. This not only solidifies your business relationships but also upholds the integrity of the GST system.

The importance of GSTR-1 extends beyond mere compliance. Proper filing helps you avoid penalties and interest on late payments, ensuring your business remains in good standing with tax authorities. This fosters trust and credibility, essential components of a thriving business.

Mastering GSTR-1 is not just about meeting legal requirements—it’s about ensuring smoother business operations and securing financial stability. In this blog, we’ll discuss GSTR 1 last date, filling date, late fee, process and other important things you need to know for a seamless compliance.

Table of Contents

Understanding GSTR-1

GSTR-1 is a crucial return that every registered GST taxpayer must file either monthly or quarterly, depending on their turnover. This return captures the details of all outward supplies (sales) made by the taxpayer. It plays a significant role in ensuring the smooth functioning of the GST system and helps maintain transparency in the supply chain.

There are in total 13 sections given in the GSTR-1. Here’s a list of all to give you a complete idea.

| Table No. | Description | |

|---|---|---|

| Tables 1, 2 & 3 | Key details including GSTIN, legal and trade names, and aggregate turnover from the previous year, forming the foundational data for accurate GST reporting. | |

| Table 4 | Detailed records of taxable outward supplies to registered persons (including UIN-holders), excluding zero-rated supplies and deemed exports, ensuring precise GST compliance. | |

| Table 5 | Documentation of taxable inter-state supplies to unregistered persons where invoice values exceed Rs. 2.5 lakh, crucial for transparency in high-value transactions. | |

| Table 6 | Reporting of zero-rated supplies and deemed exports, essential for GST benefits like export refunds and duty drawbacks, facilitating seamless international trade. | |

| Table 7 | Record of taxable supplies to unregistered persons, excluding high-value inter-state transactions, adjusted for debit and credit notes to maintain clear transactional records. | |

| Table 8 | Comprehensive overview of nil-rated, exempted, and non-GST outward supplies, ensuring compliance across varied supply categories. | |

| Table 9 | Amendments to taxable outward supplies reported in previous periods, including debit notes, credit notes, and refund vouchers, for accurate revision and reconciliation. | |

| Table 10 | Documentation of debit notes and credit notes issued to unregistered persons, ensuring transparency in adjustments to supply transactions. | |

| Table 11 | Reporting of advances received, adjusted, or amended during the current period, alongside revisions to past tax period information, for up-to-date GST records. | |

| Table 12 | Summarized HSN-wise breakdown of outward supplies, essential for compliance and statistical reporting. | |

| Table 13 | Documentation of all invoices and related documents issued during the period, maintaining a clear audit trail and meeting GST documentation standards. | |

| Table 14 | Supplier’s reporting of sales through e-commerce operators, where TCS collection or tax payment responsibilities apply under GST regulations. | |

| Table 14A | Amendments to e-commerce sales reporting, ensuring updated and accurate information in compliance with GST requirements. | |

| Table 15 | E-commerce operator’s comprehensive report on B2B and B2C sales, including TCS obligations under section 9(5) of the CGST Act. | |

| Table 15 A | Amendments to e-commerce operator’s sales reporting, specifying revisions for B2B and B2C transactions to ensure regulatory compliance. |

| Business Turnover | Month/Quarter | Due Date |

|---|---|---|

| Turnover up to Rs.5 crore (QRMP Scheme) | Oct-Dec 2023 | 13th Jan 2024 |

| Jan-Mar 2024 | 13th April 2024 | |

| April-June 2024 | 13th July 2024 | |

| July-Sept 2024 | 13th Oct 2024 | |

| Oct-Dec 2024 | 13th Jan 2025 | |

| Jan-Mar 2025 | 13th April 2025 | |

| Over INR 5 crore | Jan 2024 | 11th Feb 2024 |

| Feb 2024 | 11th Mar 2024 | |

| Mar 2024 | 12th Apr 2024 (earlier 11th Apr 2024)* | |

| Apr 2024 | 11th May 2024 | |

| May 2024 | 11th June 2024 | |

| June 2024 | 11th July 2024 | |

| July 2024 | 11th Aug 2024 | |

| Aug 2024 | 11th Sept 2024 | |

| Sept 2024 | 11th Oct 2024 | |

| Oct 2024 | 11th Nov 2024 | |

| Nov 2024 | 11th Dec 2024 | |

| Dec 2024 | 11th Jan 2025 | |

| Jan 2025 | 11th Feb 2025 | |

| Feb 2025 | 11th Mar 2025 | |

| Mar 2025 | 11th April 2025 |

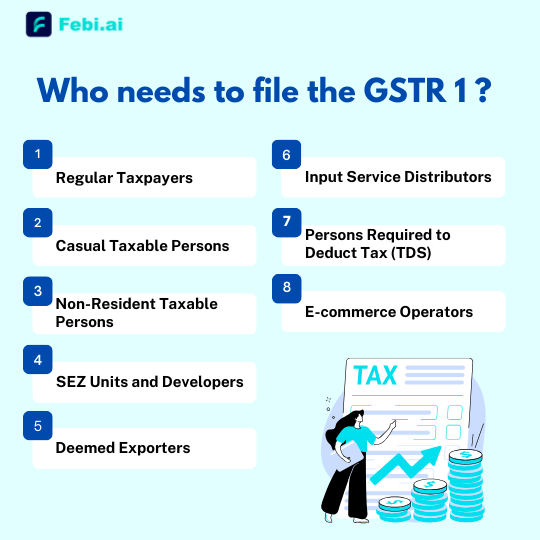

Who needs to file the GSTR 1?

The GSTR-1 is a crucial monthly or quarterly return for businesses under GST. It details all outward supplies of goods and services. The GSTR 1 return file is mandatory for:

- Regular Taxpayers: All businesses and professionals registered under GST must file GSTR

- Casual Taxable Persons: Those occasionally dealing in supplies must adhere to the GSTR 1 filing date.

- Non-Resident Taxable Persons: Non-residents providing goods or services in India need to submit the GSTR-1 return.

- SEZ Units and Developers: Special Economic Zone units and developers are required for filing of GST R1.

- Deemed Exporters: Those involved in deemed export transactions must ensure they meet the GSTR 1 due date.

- Input Service Distributors: Entities distributing input services across branches.

- Persons Required to Deduct Tax (TDS): Entities mandated to deduct tax at source.

- E-commerce Operators: Required to collect tax at source, ensuring their GSTR 1 file process is up-to-date.

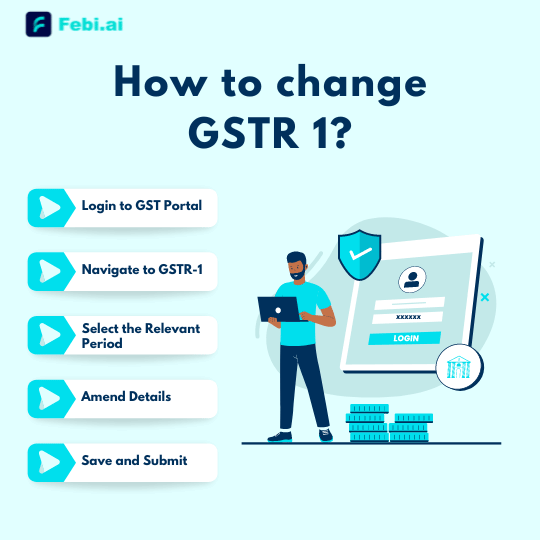

How to change GSTR 1?

Once you’ve submitted your GSTR-1, direct revisions aren’t possible. But don’t worry—corrections can still be made in future returns. Here’s a simple guide to get it right:

- Login to GST Portal: Start by accessing the portal with your credentials. It’s your gateway to managing your returns efficiently.

- Navigate to GSTR-1: Go to the ‘Services’ menu, select ‘Returns’, and then head to the ‘Returns Dashboard’. This is where the magic happens!

- Select the Relevant Period: Pick the financial year and return period for the correction. Make sure you’re editing the right time frame.

- Amend Details:

- For B2B Invoices: Use Table 9A to make necessary adjustments.

- For B2C Large Invoices: Head to Table 9B for any updates.

- For Credit/Debit Notes: Table 9C is your go-to for these amendments.

- For Export Invoices: Make changes via Table 9A.

- Save and Submit: Don’t forget to save your changes before hitting submit!

By following these steps, you can ensure that your GSTR 1 return file is accurate and up-to-date, even if there were initial hiccups. Keeping your records precise helps you avoid complications and stay compliant.

GSTR 1 late fee

Missing the GSTR 1 due date incurs a late fee for GSTR 1. Here’s the breakdown:

- For Nil Return: INR 20 per day (INR 10 each for CGST and SGST).

- For Other Returns: INR 50 per day (INR 25 each for CGST and SGST).

The maximum GSTR 1 late filing fees is capped at Rs. 10,000 per return period. Remember, there’s no late fee for IGST.

Key Dates and Reminders

- Always check the GSTR 1 last date to avoid penalties.

- Familiarise yourself with the format of GSTR1 to ensure proper filing.

- Be aware of the GSTR 1 filing last date to maintain compliance.

By adhering to these guidelines, you can streamline your GSTR 1 file process and avoid any unnecessary late fees. Keep an eye on the GST R1 due date to ensure timely compliance and smooth operations.

Conclusion

Effective GSTR-1 filing is vital for maintaining compliance and avoiding unnecessary penalties. By staying informed about filing deadlines, adhering to the correct format, and understanding the impact of late submissions, you ensure that your business operates smoothly and remains in good standing with GST regulations.

To streamline this process and keep your compliance efforts on track, explore Febi.ai’s advanced compliance calendar. Our GST calendar offers real-time updates on paid, due, and pending dates, along with instant access to critical GST reports and statements. Febi.ai’s designed to help you stay organised and proactive in managing your GST obligations. Additionally, it offers AI-powered Bookkeeping, 20+ important financial statements and reports, smart invoicing, paperless file management and several other capabilities important for business stakeholders and CFOs.

Don’t let compliance challenges hinder your business. Book a demo of Febi.ai today to discover how our innovative solutions can simplify your GST management and enhance your efficiency. Empower your business with precise, timely compliance—experience the difference with Febi.ai.

Schedule a Demo

FAQ

1. Who needs to file the GSTR-1?

2. How can I amend a GSTR-1 return?

3. What are the penalties for late GSTR-1 filing?

4. How does the format of GSTR-1 impact filing?

5. What should I do if I miss the GSTR-1 filing date?

Found this blog insightful?

Here are a few related blogs you may want to read.

Get started with Febi today

If you’re ready to take your business’s financial management to the next level with Febi.ai’s AI accounting software, reach out to our team today to schedule a demo or start your free trial!

Found this blog helpful? Share it on your socials!