Table of Contents

If you’re running a small or medium business in India, you already feel the heat. Tight margins, climbing input costs, and an endless trail of compliances – it adds up quickly. But here’s something a lot of business owners overlook – tax planning. Most treat it like a seasonal flu – shows up once a year, gets dealt with, and then forgotten. But the truth is, legal tax planning isn’t a one-time chore – it’s a smart, ongoing strategy.

And why should you care? Well, saving even 10–15% on taxes isn’t pocket change. That’s extra working capital, maybe a new hire, or just some breathing room when times get rough.

This guide is packed with practical, legal tax saving tips for small business owners who want to reduce their tax without crossing any lines. Ready to take control?

1. Maximize Business Tax Deductions

You don’t need a degree in finance to understand one basic trick – if it’s a business tax deduction, claim it. Seriously, this is low-hanging fruit.

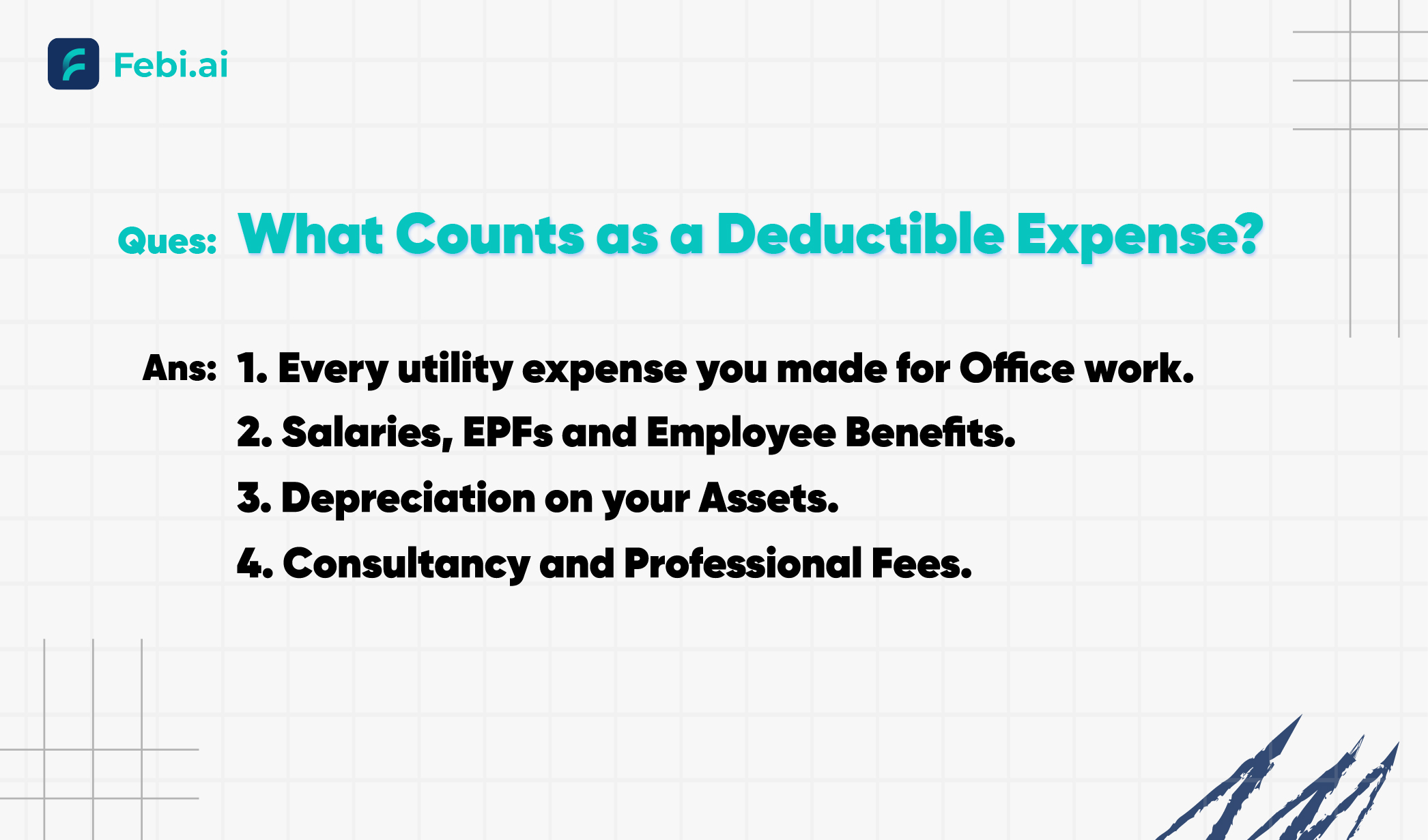

Know What Counts as a Deductible Expense

Coworking rent? Yep. Website domain renewal? Also yes. Anything that’s solely for your business – but not your Sunday Netflix – could be claimed under Section 37(1). A few examples:

- Electricity or broadband for office

- Toll and fuel for business travel

- Airfare and client lunches

- Subscription tools like Canva, Febi.ai, Zoho, QuickBooks

Salaries, EPF, and Employee Benefits

If you’ve got a team, you’ve got tax-saving potential. You can deduct:

- Regular salaries and allowances

- EPF contributions

- Staff bonuses or performance pay

- Gratuity (under Section 43B)

These aren’t just good management practices – they’re strategic tax decisions too.

Depreciation: Your Asset’s Hidden Superpower

Buy a laptop or delivery van for business? You can claim depreciation under Section 32. Spread the asset’s cost across its useful life and lower your profits – legally.

- Depreciation rates range from 15% to 40%

- Bonus: 20% additional depreciation if installed before 30th September in manufacturing

Your tech investments could shave lakhs off your taxable income.

Professional and Consultancy Fees

Hired a lawyer for a contract? A CA for GST filing? Paid for legal help through an app? All of that counts as a business tax deduction. Don’t leave it on the table.

2. Use Deferred Tax Strategies (Without Overthinking It)

Most small businesses miss out here – not because they don’t want to save, but because the term “defer tax liability” just sounds… complicated.

So, What Is Deferred Tax Liability?

Let’s say you buy machinery and claim full depreciation in your income tax, but show only 20% in your accounting books. This difference in timing is deferred tax liability.

In simple words? “I’ll pay this tax later. Not now.”

It gives you extra breathing space in the short run.

Deferred Tax Asset: Flip Side of the Coin

Imagine you had losses this year. You can carry them forward for up to 8 years and offset them against future gains. That’s a deferred tax asset.

Or maybe you paid Minimum Alternate Tax (MAT) under Section 115JB even though your regular tax was zero. That MAT can be carried forward for up to 15 years as credit.

Learn to play the deferred tax game smartly and have long-term gains.

Quick Example, So It’s Crystal Clear:

You buy a ₹10 lakh machine.

- You take 100% depreciation under the Income Tax Act.

- You show only 20% in your accounting books.

Now? You saved tax now, but you’ll pay a bit more in future years – that’s deferring your liability.

If you ran a loss or paid MAT this year, boom – you’ve just created a deferred tax asset.

3. Pick a Tax-Smart Business Structure

What you choose to call your business – whether sole proprietor, LLP, or Pvt Ltd. It can seriously change your tax bill.

Tax Rates Based on Entity Type

| Entity Type | Tax Rate (FY 2025-26) |

|---|---|

| Sole Proprietor | Regular Individual slab (up to 30%) |

| Partnership/LLP | 30% + surcharge + cess |

| Private Ltd | 22% + surcharge + cess |

Choose wrong, and you might be burning money on higher tax and unnecessary compliances.

Use Presumptive Taxation (If You Qualify)

Turnover under ₹2 crores? Or ₹50 lakhs if you’re a professional? Then:

- Declare profits at 8% or 50% under Section 44AD/44ADA

- Skip audits, forget book-keeping nightmares

For consultants, freelancers, and local shop owners – this one’s a goldmine.

Audit Compliance Made Easy

Presumptive taxation = fewer headaches. No audits, no tedious monthly books. For any business under ₹2 crore, this is one of the easiest tax saving tips for small business.

4. Put Your Money in Tax-Saving Instruments

Old tricks. Still work.

80C Still Packs a Punch

Up to ₹1.5 lakh deduction under Section 80C if you invest in:

- PPF (safe and steady)

- 5-Year FDs (locked but tax-saving)

- ELSS (equity mutual funds with benefits)

- Life insurance policies

These aren’t just tax savers. They’re also long-term wealth tools.

Beyond 80C: Other Powerful Sections

- 80D: ₹25,000 (or ₹50K for seniors) for health insurance

- 80G: Donations to eligible NGOs (50–100% deduction)

- 80E: Education loan interest? Yes, that too is covered

Save taxes while doing something meaningful. It’s a win-win situation.

Invest in Innovation: Section 35

If your business does R&D – think product innovation, tech upgrades – you could claim 150% weighted deduction.

Perfect for:

- Tech Startups

- Pharma companies

- Clean energy or Agri-tech businesses

If you’re building the future, you deserve some tax love.

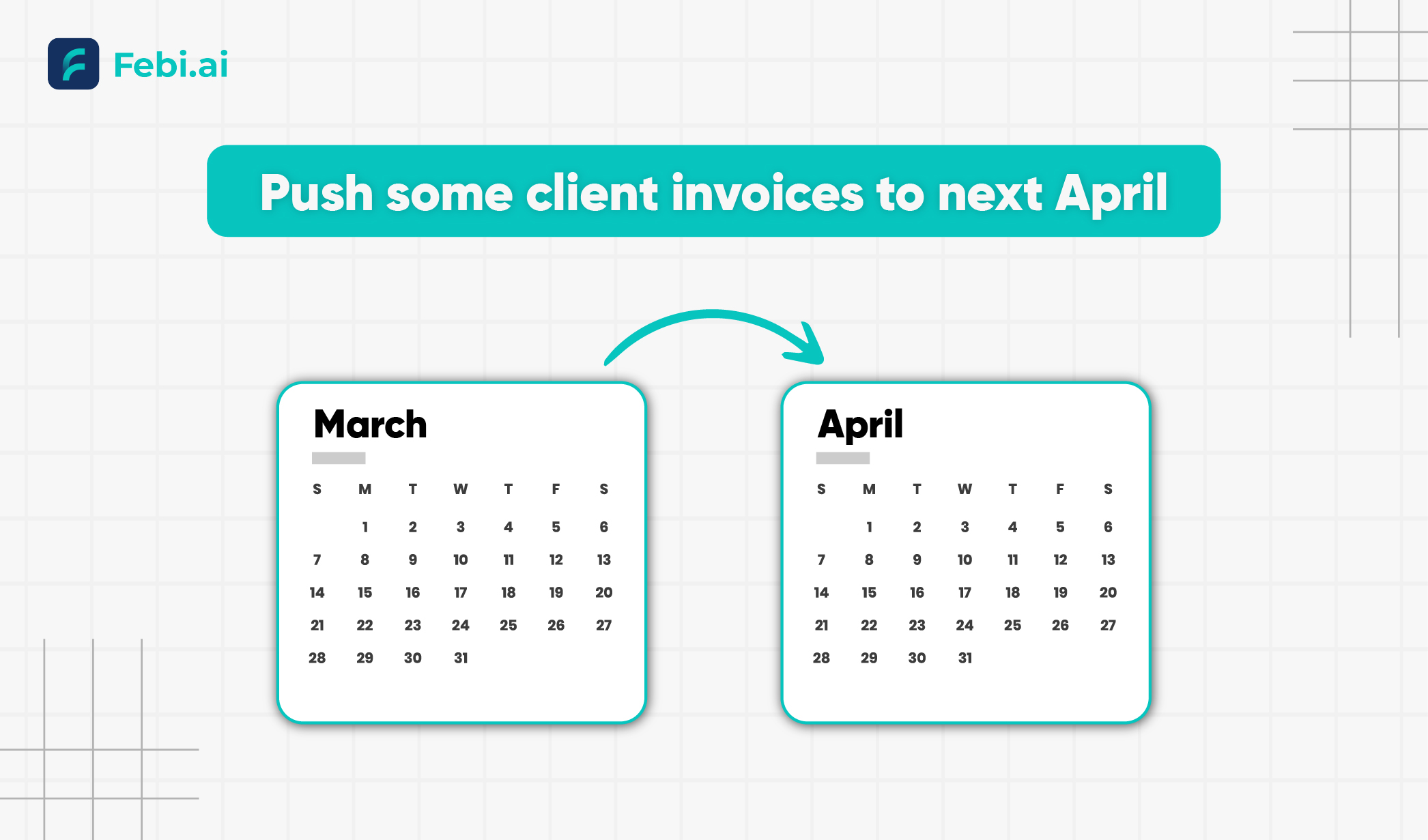

5. Time Your Income and Expenses Right

Sometimes, the best tax saving tips for small business are hiding in the calendar.

Shift Income or Prepay Expenses

Got a great year in profits? You could:

- Push a client invoice to next April

- Prepay rent, subscription software, or maintenance

Less profit this year = less tax now.

Build a March Checklist

Before March 31st:

- Book pending expenses

- Pay staff bonuses

- Create gratuity or leave provisions

- Write off bad debts

Just by syncing actions with timelines, you could save lakhs – legally.

Common Tax Blunders (And How to Avoid Them)

- Claiming your personal Netflix as a business tool? Not smart but a foolish act.

- No bills or payment proofs? You will face problems in Audit.

- Missed advance tax payments? Hello, Section 234B/C penalties.

Stay on top of compliance with Febi.ai or get ready for sleepless nights.

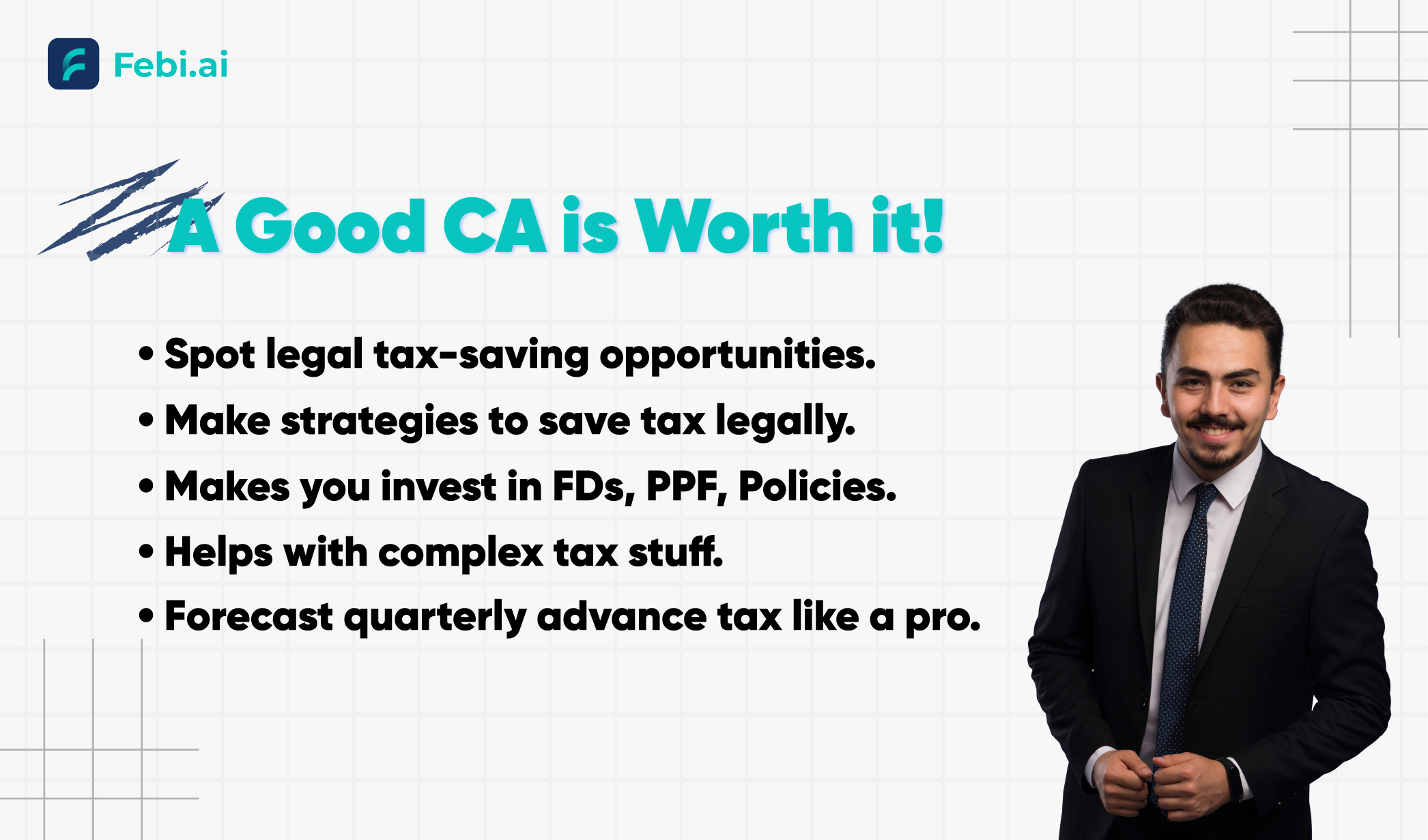

Why a Good CA Is Worth It

A Chartered Accountant isn’t just a tax-filer. They’re your guide through India’s tax jungle.

They can:

- Spot legal tax-saving opportunities

- Make strategies to save tax legally

- Make you invest in different ways which can save tax like FDs, PPF, Policies.

- Help with complex stuff like deferred tax asset and liability

- Forecast quarterly advance tax like a pro

A good CA won’t cost you. They’ll probably save you way more than their fee.

Wrapping It All Up

This isn’t about tax evasion. It’s about knowing your rights and using them wisely. With the right mix of business tax deductions, clever use of deferred tax asset and liability, and timing your decisions, you can genuinely lighten your tax load.

Just don’t leave it till the last minute.

Start early. Plan wisely. Save legally.